Kosamattam Finance is looking to raise up to Rs 300 crore through secured redeemable non-convertible debentures (NCD) offering interest of 8.30% – 10.47% for different maturities. Kosamattam Finance (KFL) is a systemically important non-deposit taking NBFC primarily engaged in the Gold Loan business, lending money against the pledge of household jewellery (“Gold Loans”) in the state of Kerala, Tamil Nadu, Karnataka, Andhra Pradesh, Delhi, Maharashtra, Gujarat and Telangana along with the Union Territory of Puducherry.

Key Features for Kosamattam Finance (KFL) NCD

| Issue Open Date | 30 Aug 2021 |

| Issue Closing Date | 24 Sep 2021 |

| Type of Instrument | Secured redeemable NCDs |

| Size of issue | Rs 300 crores (Base size: Rs 150 crores) |

| Minimum Investment | 10 NCD (Rs 1000 per NCD) |

| Max Investment | N/A |

| Listing | BSE, |

| Credit Rating | BWR BBB + Outlook Stable by Brickworks Ratings |

| Interest | Monthly and Cumulative |

| Allocation method | First Come First Serve Basis |

| NRI allowed? | Not eligible |

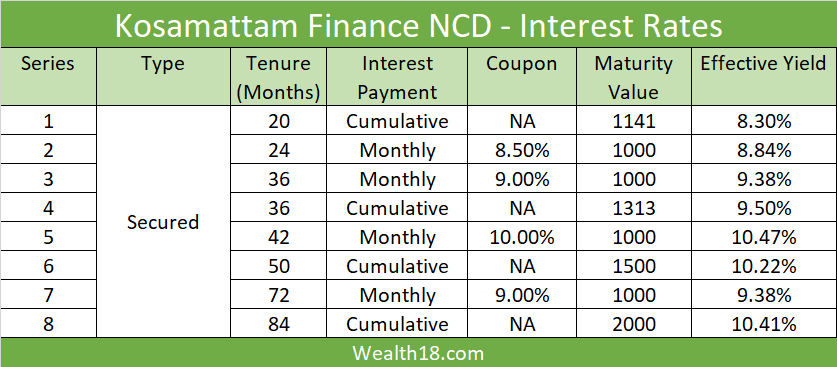

Interest Rate options for Kosamattam Finance NCD Sep 2021

There are no PUT & Call options for these Secured NCDs. (which means the NCD issuer cannot redeem before bond’s maturity and the investor cannot sell the bond to the issuer. Investor can however sell the bonds in the secondary market on exchanges.

About Company and NCD Issue

Kosamattam Finance Ltd. (KFL) is a systemically important non-deposit taking NBFC primarily engaged in the Gold Loan business, lending money against the pledge of household jewellery (“Gold Loans”) in the state of Kerala, Tamil Nadu, Karnataka, Andhra Pradesh, Delhi, Maharashtra, Gujarat and Telangana along with the Union Territory of Puducherry.

This is the 23rd Debt offer from the company since April 2014. It is IRDA registered composite corporate insurance agent. Kosamattam also holds SEBI registration as depository participant and FFMC to act as money changer. KFL is also an AMFI registered mutual fund advisor and also holds registration from LEIL. The last offer was in the month of March 2021.

In addition to the core business of Gold Loan, KFL also offer fee based ancillary services which includes Microfinance, money transfer services, foreign currency exchange, power generation, agriculture and air ticketing services. Thus it has diverse business activities now.

As on June 30, 2021, it had a network of 974 branches spread in the states of Kerala, Tamil Nadu, Karnataka, Andhra Pradesh, Delhi, Maharashtra, Gujarat and Telangana along with the Union Territory of Puducherry and employed 3,130 persons in business operations. The company belongs to the Kosamattam Group led by Mathew K. Cherian with a headquartered in Kottayam in the state of Kerala.

Financials

For the last three fiscals, the company has posted total income/net profits of Rs. 475.36 cr. / Rs. 43.15 cr. (FY19), Rs. 499.33 cr. / Rs. 47.63 cr. (FY20) and Rs. 542.26 cr. / Rs. 65.32 cr. (FY21). Thus it has shown gradual growth in its top and bottom lines.

KFL’s net NPAs declined over the periods from1.28% in FY19 to 0.86% in FY21. As of March 31, 2021, its current paid up equity capital of Rs. 202.50 cr. is supported by free reserves of Rs. 318.08 cr.

Its debt equity ratio of 6.64 as of March 31, 2021 will rise to 7.21 post this debt issue.

Taxation Aspect

Interest:

-

- The interest earned is to be added to one’s total income, and hence is entirely taxable as per one’s income tax slab.

- NCDs taken in the DMAT form will NOT attract any TDS on the interest income. However, if NCD are taken in physical form, TDS will be applicable if the interest amount exceeds Rs. 5,000. Investors, if eligible, can submit For 15 G/H to avoid TDS.

Taxation for Cumulative Interest Option:

For the cumulative option, you do not get periodic (monthly / annual ) interest. Instead you get a lumpsum amount at the maturity period. Investors are often confused if this cumulative interest received on maturity is to be treated as a capital gain or interest income. Many advisors incorrectly mis-sell saying that the income from cumulative option can be treated as Capital Gain rather than Interest income.

Note that even for Cumulative option, the amount should be treated as Interest income. This was also clarified by the experts at Moneycontrol.

| Income | Taxation |

| Interest earned on NCD | Taxable as per tax slab of Investor |

| If sold on exchange (before 12 months) | Short term capital gain / loss Taxable as per tax slab of Investor |

| If sold on exchange (after 12 months) | Long term capital gain / loss Taxable @ 10% without indexation

In case of an individual or HUF, being a resident, where the total income as reduced by such long-term capital gains is below the maximum amount which is not chargeable to income-tax, then, such long-term capital gains shall be reduced by the amount by which the total income as so reduced falls short of the maximum amount which is not chargeable to income-tax and the tax on the balance of such long-term capital gains shall be computed at the rate mentioned above. |

Tax Saving in case of Long term capital Gains

| By investment in Capital Gain Bonds | Under Section 54EC of the I.T. Act, long term capital gains arising to the debenture holders on transfer of their debentures in the company shall not be chargeable to tax to the extent such capital gains are invested in certain notified bonds within six months after the date of transfer. |

| By investment in residential property | As per the provisions of Section 54F of the I.T. Act, any long-term capital gains on transfer of a long term capital asset (not being residential house) arising to a Debenture Holder who is an individual or Hindu Undivided Family, is exempt from tax if the entire net sales consideration is utilized, within a period of one year before, or two years after the date of transfer, in purchase of a new residential house, or for construction of residential house within three years from the date of transfer |

How to Apply

- Online – You can invest online in DMAT form through your online share trading account or through your broker.

Comparison

There are other NCDs available in the secondary market that are giving better yield (YTM). However, these NCDs have lower balance duration and the purchase will incur small brokerage cost.

https://www.nseindia.com/live_market/dynaContent/live_watch/equities_stock_watch.htm?cat=SEC

Select – “Bonds in CM”

https://www.bseindia.com/markets/debt/tradereport.aspx

Positive factors of this NCD

- Attractive Interest rates of 10.47% in the market where the interest rates are declining.

- It is secured NCD, so at least it is safer than unsecured NCD. If case the company shut down for any reason, the NCD investors will get the preference in repayment (as the NCD is secured and backed by the assets of the company).

Negative factors of this NCD

- NCDs are not risk free and have default risk. It has poor rating (BBB+)

- NCDs are not very liquid so it will be difficult to sell it before maturity. Though they are listed on exchanges but trading volumes are low to get right price.

- As the interest is taxable, post tax returns may not be comparable to the tax free bonds (if you are in higher tax bracket). It may be better to opt for the cumulative option.

The interest on NCDs is taxed at the slab rate. Hence, investors in the highest tax bracket of 30% are likely to get a post-tax yield of 7.33%. So you can opt for Debt funds that offers diversity.

Summary

- Attractive Interest: Investors who are willing to take high risk can consider this NCD. As the rating is BBB+, investors should be careful if making this investment.

- Capital Gain: If the interest rates fall (most likely), these bonds are most likely be traded at premium, thereby having chance of capital gain as well (in addition to the coupon interest). However, the interest rate are already very low and chances of further reduction is less.

Though the interest rate is quite attractive, remember that the NCDs are not very liquid in the market. If you are ready to lock in money for that duration without much risk, then you can go for these NCD. Also, note that the NCD interest is taxable, so investor in higher tax brackets need to consider the post tax returns.

If you looking for Debt instruments only, then you can consider investing in Debt mutual funds, PPF etc. If you are looking for better returns over long term, you should consider investing in Equity Mutual funds.