SREI Equipment Finance will open its public issue of NCDs on 3rd Jan 2017 & it closes on 20th Jan 2017. This NCD issue is offering yield upto 9.7% and have 7 different investment options.

Latest NCD issue of Reliance Home Finance (22nd Dec 2016) was over-subscribed 3 times the issue size on day one itself.

In this post, I am trying to put details around how good this SREI Equipment Finance NCD is ? What are the postive and negative factors of SREI Equipment Finance NCD? Who should invest in SREI Equipment Finance NCD?

Key Features of SREI Equipment Finance NCD

- NCD Issue Open: 3-Jan-2017

- NCD Issue Closing date: 20-Jan 2017

- Type of Instrument: Secured redeemable non-convertible debentures (NCD) for 3 & 5 years

- Size of Issue: Rs. 250 crores with a green-shoe option of another Rs 500 crores = Total Rs 750 crores

- Minimum & Maximum Investment: minimum 10 NCD of Rs 1000 each = Rs 10000.

- Listing: Proposed to be listed on NSE & BSE (within 12 working days of closing the issue)

- NRI– Non Resident Indian (NRI) cannot invest in this issue

- Credit Rating– BWR AA+ – Outlook Stable by Brickwork Ratings & SMERA AA/Stable’ by SMERA Ratings Ltd

- Interest Payable – Monthly, Annual & Cumulative (on maturity date of NCDs).

- Issue Allocation or Allotment method: First come first served basis

- Issue Breakup

| Category | Allocation | Priority |

| Individual Retail & HNI | 50% | 1st |

| Others | 50% | 2nd |

| TOTAL | 100% |

There are no PUT & Call options for these Secured NCDs. (which means the NCD issuer cannot redeem before bond’s maturity and the investor cannot sell the bond to the issuer. Investor can however sell the bonds in the secondary market on exchanges.

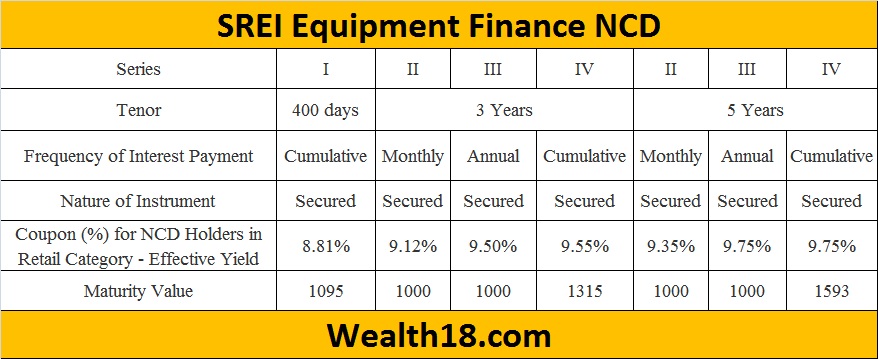

Interest rate options for SREI Equipment Finance NCD

About Company

- SREI Equipment Finance is one of the leading NBFC in organised equipment financing

- The company provide financial products and services to companies operating in the construction, mining, technology and solutions, healthcare, ports and railways, oil and gas, agriculture and transportation sectors. Financial products and services comprise loans, leases, rentals and fee-based services.

- As of September 30, 2016, the company have presence in approximately 21 states, including 89 branches across India.

Taxation Aspect

NCDs taken in the DMAT form will NOT attract any TDS on the interest income.

However, if NCD are taken in physical form, TDS will be applicable if the interest amount exceeds Rs. 5,000.

| Internest earned on NCD | Taxable as per tax slab of Investor |

| If sold on exchange (before 12 months) | Short term capital gain / loss Taxable as per tax slab of Investor |

| If sold on exchange (after 12 months) | Long term capital gain / loss Taxable @ 10.30% without indexation

In case of an individual or HUF, being a resident, where the total income as reduced by such long-term capital gains is below the maximum amount which is not chargeable to income-tax, then, such long-term capital gains shall be reduced by the amount by which the total income as so reduced falls short of the maximum amount which is not chargeable to income-tax and the tax on the balance of such long-term capital gains shall be computed at the rate mentioned above. |

Tax Saving in case of Long term capital Gains

| By investment in Capital Gain Bonds | Under Section 54EC of the I.T. Act, long term capital gains arising to the debenture holders on transfer of their debentures in the company shall not be chargeable to tax to the extent such capital gains are invested in certain notified bonds within six months after the date of transfer. |

| By investment in residential property | As per the provisions of Section 54F of the I.T. Act, any long-term capital gains on transfer of a long term capital asset (not being residential house) arising to a Debenture Holder who is an individual or Hindu Undivided Family, is exempt from tax if the entire net sales consideration is utilized, within a period of one year before, or two years after the date of transfer, in purchase of a new residential house, or for construction of residential house within three years from the date of transfer. |

How to Apply

- Physical Form – You can download the Form and submit to designated bank branches alongwith cheque. (Link to download SREI Equipment Finance Jan 2017 Form)

- Online – You can invest online in DMAT form through your online share trading account or through your broker.

Comparison

There are other NCDs available in the secondary market that are giving better yield (YTM). However, these NCDs have lower balance duration and the purchase will incur small brokerage cost.

Positive factors

- Attractive Interest rates of 9.75% as compare to Banks FD rates (approx 8%)

Negative factors

- NCDs are not very liquid. Though they are listed on exchanges but trading volumes are low to get right price.

- For an investor in the highest tax bracket, it doesn’t make sense to invest in these as the net returns are comparable with that of the tax-free bonds.

Summary

- Attractive Interest: Investors who are looking for steady income can go for this NCD as the Interest rate is attractive and rating is AA.

- Capital Gain: If the interest rates fall (most likely), these bonds are most likely be traded at premium, thereby having chance of capital gain as well (in addition to the coupon interest).

Though the interest rate is quite attractive, remember that the NCDs are not very liquid in the market. If you are ready to lock in money for that duration without much risk, then you can go for these NCD.

If you looking for Debt instruments only, then you can consider investing in Debt mutual funds, PPF etc

If you are looking for better returns over long term, you should consider investing in Equity Mutual funds.