Bank Fixed Deposits are one of the most popular investment avenue for risk averse Indian investors. With benefits such as -decent interest rates (9 – 10%), capital safety, bank reputation, accessibility etc., it may seem to be good option.

However, a prudent investor should carefully consider all the aspects before taking the investment decision.

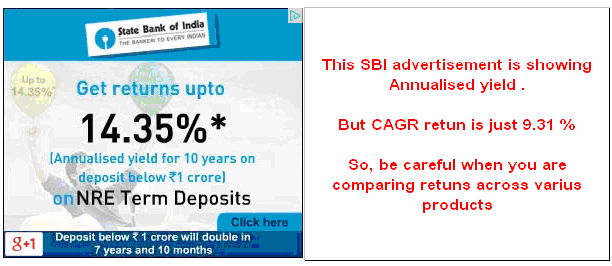

1) Advertised Bank FD yield may be misleading

In recent times, many banks in their advertisement show the Annualised yield from FD, which is misleading. For e.g in below SBI advertisement, you can see that SBI is advertising that you are getting annualised yield of 14.35% over 10 years.

You may think it is better option as compared to PPF (giving 9%) or some Mutual funds who are giving 11-13% return.

Well, you may be incorrect in thinking that.

It is the way bank is showing the yield calculation which may be different from other products.

Mutual funds show CAGG return (Compounded Annual Growth return) which is different from above advertised annualised return

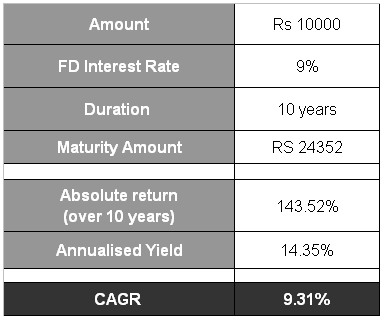

SBI is offering 9% interest on their FD. If you deposit Rs 10000 for 10 years, your maturity amount will be Rs 24352 . They are calculating, annualised yield as 14.35%

BUT, the CAGR return is just 9.31% (not 14.35% as you might think)

2) Liquidity Issues / Pre-mature Penalty

Bank FDs are not very liquid. Yes you cat get the money if you want it before maturity. But you pay a cost for that. (known as pre-mature penalty)

Many big banks charge 0.5-1% penalty for pre-mature withdrawal of FD. You may also get the lesser interest as applicable for lower duration

Interest Rates for Premature withdrawal of FDs = Interest Rate applicable for actual period of FD as per the rates prevalent at the time of investment – penalty (0.5-1%)

For e.g.

6 months rate – 8.50% , 1 year rate – 9%

You make FD of Rs 10000 for 1 year (applicable rate 9%)

You need money after 6 months and intend to break that FD.

You will get following interest rate :

Interest rate applicable for actual duration (6 months) 8.5% Minus penalty of 1% = Net Interest rate applicable will be 7.5% p.a.

So it is advisable to split amount into multiple FD in the first place, so that if you need money, you donot need to break whole FD.

3) Interest on Bank FD is TAXABLE – so compare Post tax returns for decision

Many times people do not think of applicable taxes when comparing two investment products.

For 30% tax slab investor, FD @ 9% interest will just give post tax return of 6.22%

Regarding Bank FD Interest, there are following 2 points to consider

a) Interest on Bank FD is TAXABLE & you need to show it under “Income from Other Sources” while filing Income Tax return and it will be taxable as per your applicable tax slab.

There is no threshold; even Rs 1 earned from Bank FD is taxable.

b) Bank may deduct TDS @10% if the total interest in one financial year is more than Rs 10000. If your PAN is not updated in your account, bank may deduct TDS @20%

However, if your total income from all sources is below taxable limit, you may submit Form 15G/H to bank to apply for non-deduction of TDS. See – who can submit Form 15 G / H

Read My post – How to avoid TDS on Bank FD Interest

c) So if you have FD in 2 banks, and interest is Rs 7000 in each bank. Bank will not deduct TDS as it is less than Rs 10000.

However, you still need to show Rs 14000 in your Income Tax return and pay tax as per your tax slab.

So your real post-tax return will be as follows : If your FD interest rate is 9%, then post –tax return is

So , please compare the post-tax return of different products, before making any decision.

4) Sometimes, even normal Saving Account can give better returns than FD

Some banks are offering 7% interest in their Savings Account (for e.g Yes Bank)

See from table above, the post tax return is higher in that saving account than in FD .

Please note that this comparison will be valid only for Saving accounts offering 7% interest & where Interest earned in Saving account is less than Rs 10000 (Investment upto Rs 140000)

u/s 80TTA, You can claim upto Rs 10000 for Saving Bank Interest. Read the post

Summary

If you are in high Tax slab (30%), Bank FD may not be tax efficient option for you. Also you can keep some money in High Interest Saving account & get tax free Income upto Rs 10000.